Though CBA has intensified its thrust into the business banking current market, Chesler suggests there is limited likely for banking institutions to offset weakness in mortgages right away.

“The difficulty is there is only so numerous businesses you can lend to, they’ve normally been in that industry,” he claims.

Barrenjoey analyst Jon Mott suggests banks experienced grow to be extra highly-priced as investors cycled into them as defensive stocks, centered on expectations for modest interest fee will increase in advance of this week. But the shock 50 basis issue maximize by the RBA on Tuesday implies this is now getting unwound.

“We estimate this week’s correction in bank share charges reflects an boost in the stagflation/recession scenario from all-around a zero to 5 per cent chance to all-around a 10 to 15 per cent likelihood,” Mott states.

“This scenario is not dissimilar to the derating viewed in the US banking institutions this calendar year as the chance of a US recession rose and started to be factored into bank share rates.”

Analysts raised thoughts in excess of the scale of the banks’ exposure to mortgages, with one particular pointing out the banks’ merged $3 trillion equilibrium sheet simply cannot be simply redirected into business banking, declaring that when in 1986 two-thirds of all Australian financial loans have been to enterprises, in 2022 two-thirds of all loans are for mortgages.

The banks’ moves to “double down” in mortgages considering that the royal fee and ditch growth businesses will make it even much more challenging for them to come across expansion options outside of property supplied the dimension of their present harmony sheets.

“Australia demands to move absent from buying up rocks and building homes,” claims a single analyst.

“Moving into and lending to smaller corporations that can produce careers and progress has to be the answer, but there’s absolutely nothing they can do. They’ve jumped out of the plane already and want to hope the parachute will work, since they are falling with no exit system.”

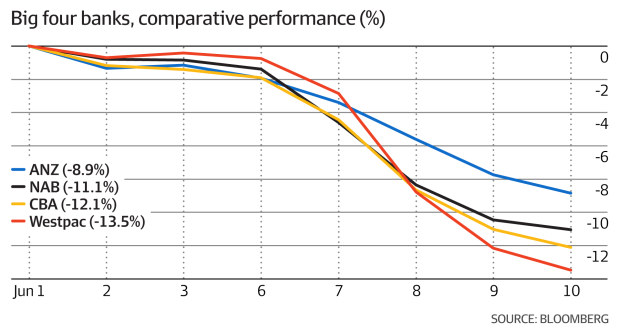

Although the financial institutions recovered ground in early buying and selling in opposition to a gloomy market place in early morning investing on Friday, with ANZ Lender bouncing of a 12-month small and Commonwealth Lender, Westpac and Countrywide Australia also rebounding, concerns about their hefty valuations saw them surrender gains.

VanEck main expenditure officer Arian Neiron says the trend of banks’ outperformance, having obtained 3.41 for each cent versus a 1.27 for each cent slide in the S&P/ASX 200 Index in the year to the end of May, is obviously staying challenged.

“This has now reversed in June just after the selection of the RBA to enhance fees by 50 basis factors,” he states.

“In June so far banking institutions have underperformed the broader share marketplace by 5.16 per cent, which represents a reasonable re-score of financial institution shares.”

Chesler claims Aussie banking companies glimpse pricey in contrast to their global peers and there are escalating anticipations that as premiums increase, their dividend yields will fall.

Strain on dividends

“We unquestionably assume that dividends could arrive less than strain on the banking aspect and at the exact time you are seeing curiosity costs keep on to go up,” he claims.

Analysts keep on to pressure that even if undesirable money owed really do not spike, the decades of solid earnings expansion will be tempered by the downturn in housing markets, leaving their share prices with much more room to drop.

UBS, Morgan Stanley, JP Morgan and VanEck have all pointed out that CBA is the most overvalued of the Aussie banks. VanEck ranks it the 3rd most costly lender of 67 banking companies globally, with a forward cost-to-earnings several of 17.85 times and a selling price to reserve of 2.32 moments.

“CBA also has the largest publicity to residential mortgages and is thus the most vulnerable to credit history development contracting and to climbing default costs which could follow the rapid maximize in home finance loan fees which commenced in May possibly, while provision for uncertain money owed are appreciable,” it said in a notice.

Most analysts and fund administrators agree that even if undesirable money owed spike the banking companies will be able to face up to the shock without having substantially impression on their earnings. UBS analyst John Storey factors out they nevertheless have $1.9 billion in collective

provisions to create again just before just about anything starts off to display up.

Chesler claims the fears about bank earnings relate far more to the point that their valuations are not heading to be matched by earnings progress.

“It’s more the expansion slowing tale [than a potential for bad debts]. Individuals are even now fully utilized, labour marketplaces are continue to really restricted, wages aren’t likely up a whole lot and inflation is, which is a slight destructive,” he claims.

“But it is not like the GFC of 2007 and 2008, we’re definitely not back in that placement. But what it is seriously saying is that lender valuations look as well high for the place we are at the second.”

MST Marquee strategist Hasan Tevfik factors out that corporate lending in Australia has fallen by the wayside and an overdue pullback in the property finance loan marketplace ought to give the financial institutions pause to look at deepening the corporate debt marketplace.

But Hugh Dive, main financial commitment officer at Atlas Money Administration, is additional optimistic on the banks’ functionality by means of the slump in housing because they’re not as uncovered to company personal debt this time about.

“There are far less undesirable corporate money owed looming,” he suggests. “It’s a small bit diverse with a lot of the company lending in that it’s gone offshore, as opposed to in earlier cycles, simply because the banks can not provide the tenors they have to have.

“The banks have historically favored to be in that house loan market place due to the fact it carries a great deal decreased personal loan losses.”

Mott suggests the banks’ share rates are likely to keep on being volatile and may perhaps come across a flooring close to phrase, but it is far too quickly to watch it as a acquiring option offered historical derating of PEs.

“We feel the time to invest in the banking companies is when the stagflation/recession state of affairs methods consensus and the financial institutions are investing at content discounts to their historic multiples,” he suggests.

“At that phase we imagine there may possibly be materials income to be manufactured in the banking companies.”